Cash Flow Planning for Mid-career Professionals

Your financial journey has a lot of milestones and transitions along the way. However, it generally breaks down into stages in which your needs, goals, and risk profile may look different than in earlier or later stages.

The midpoint of your career, when your income has increased, and you have some visibility into your likely earnings trajectory, usually corresponds to other responsibilities. These may include home ownership, creating a family, saving for kids’ education, and increasing retirement savings. And, of course, higher income means higher taxes.

Creating a flexible financial plan that protects your family, grows your assets, and minimizes is the foundation of building wealth. At this stage, you are starting to accumulate enough that mistakes and missed opportunities can be very costly.

Cash flow planning is the foundation of your financial plan, and it needs to be specific to the stage you are in.

Understanding the Planning Mindset

While budgeting is part of cash flow planning, the goals of each are very different. Budgeting is about making choices to keep spending in check, with almost a scarcity mindset. It is about current expenses and works best over a short-term time horizon. Cash flow planning looks at the short-term and the long-term. It is a tool to help you make decisions that will help you achieve future goals.

The process helps you identify future income and expenses and plan for big-ticket items. The result becomes part of your financial plan and dictates changes to across your financial plan. Understanding and detailing your flows keeps your investments tracking. It ensures you are realistic about return opportunities and gets you thinking big picture, including minimizing taxes and protecting your assets.

Getting Into the Process and Tactics

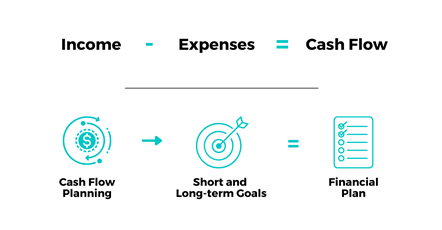

Income minus expenses equals cash flow. It’s as simple as that.

Start With Your Income

This means monthly net income after taxes, across all sources, including salary, rental income, reliable investment income, etc.

Identify Your Expenses

These usually break down as follows:

- Debt including credit cards, leases, mortgage payments, and loans (personal, education, etc)

- Taxes except for salary taxes, which is covered in net income

- Basic monthly expenses: Rent, food, gas, cable, phone, etc.

- Discretionary expenses: Dinners, trips, purchases

- Savings: Cash reserve savings, retirement or education savings, big-purchase savings

- Insurance costs: Home, health, professional liability, auto, potential umbrella policy

- Extraordinary expenses: Anything out of the norm – vet bill, car repair, etc. To get a realistic annual figure, average the last three years of these

Set Clear Goals

Spend some time identifying short- and long-term goals over a 5-10 year time horizon and then assign spending targets to them. These could be education savings, second home, home improvements, early retirement, starting your own business, etc.

Developing and working towards goals is the essence of cash flow planning. While budgeting operates from a scarcity mindset of cutting expenses, cash flow planning opens up the horizon to allow you to see clearly where you are now and where you want to go.

The purpose behind identifying both short-term and long-term goals is that the ends to achieve them are different.

Deploying Your Cash Flow Planning Strategy

The planning part links your cash flow to your future expenses, to help you achieve your goals. The process uses the outcome of your cash flow planning to create a road map to get to each goal. Different strategies are devised for each to guide better outcomes. When done correctly it can uncover gaps in your financial plan. For example:

- Are you taking enough investment risk with your investments, whether in your retirement accounts or taxable accounts?

- Should you refinance debt?

- Are you saving enough for retirement?

- Are you minimizing your taxes through tax-advantaged saving vehicles like health spending accounts and 529 plans?

- Should you diversify your income stream or invest in more tax-efficient sources of income, such as real estate?

When deploying your cash flow planning strategy, it’s essential to do check-ins against your goals and tactics to get you there. As part of your cash planning review, you should look at ways to automate as much as possible. Getting the right systems in place can ensure you hit savings goals and save as much as possible for retirement.

The Takeaway

As your financial journey unfolds, it’s important to ensure that it keeps up with your life. As you change and grow, your goals will evolve, and your resources often increase. Ensuring that your planning matches your life stage is critical to growing wealth and staying on track as you move forward.

This work is powered by Seven Group under the Terms of Service and may be a derivative of the original. More information can be found here.